May 14, 2026

BlogMicrosoft’s Multiple Equivalent Offer: Avoiding the Renewal Trap

If your Enterprise Agreement is up in the next twelve months, your Microsoft account team is going to put a Multiple Equivalent Offer (MEO) on the table. They will pitch this MEO (sometimes also called Multiple Equivalent Simultaneous Offer) as an upsell that the account team intends for you to perceive as more value at roughly the same cost.

That framing is the bait. It is also a category error. The MEO is not a pricing proposal. It is a leverage-removal mechanism, and the discount you see up front is paying for the disarming of your next renewal — the one after this one — when the price is at its peak in the exit year and your ability to walk away is gone.

What the MEO Actually Looks Like on the Table

Here’s the scenario: The Microsoft pitch deck arrives later than it should, and it’s crunch time with an expiring EA pending. Your team is frustrated and under pressure. Buzzwords appear throughout the deck: Digital Labor, Agentic AI, Frontier Firm, and Copilot Augmentation. They are the tell. Anything good for you, in the account team’s framing, is described in those terms; anything you actually asked for is described as your “historical footprint” and quoted at full Estimated Retail Price (ERP) Level A “equity” pricing, plus the 8%–35% post-July 2026 price increases fully baked in.

Your bill of materials is treated as a curiosity rather than a starting point. The amendment requirements you sent in writing get acknowledged but not addressed. The proposal does not respond to your stated requirements. It responds to the account team’s compensation plan.

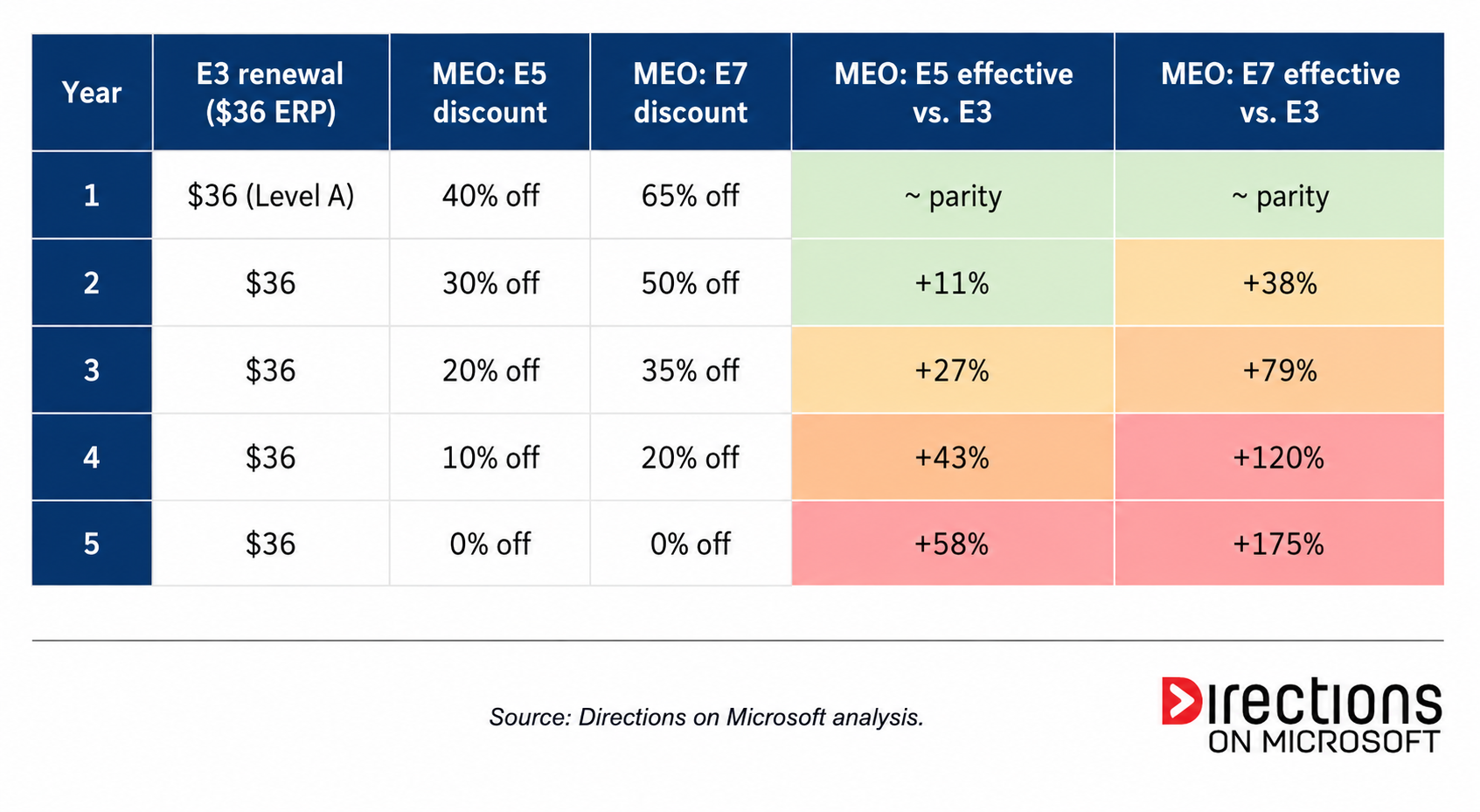

Sitting next to that obligatory undiscounted “business as usual” tab are the “rational alternatives.” The MEO arrives with three columns: Your E3 renewal at zero discount, an E5 path at 40% initial discount, and an E7 path at 65%. (If you’re renewing E5, then that gets a goose-egg discount, and E7 is your next Frontier.)

The Year One total of the next higher E-tier is engineered against the price offered on your current estate and lands near your business-as-usual price. E7 lands near it too, just from a higher list price with greater discounts. You are supposed to look at the deck and feel like you have a choice. There are three offers, take your pick, all roughly equivalent at signing.

That equivalency is the first fabrication, and it’s a more sophisticated one than it used to be. The columns aren’t equivalent on any axis except the Year One number, and the Year One number is engineered to be equivalent across all three columns precisely so that the comparison stops there. The MEO’s first letter has come to mean what it says. There really are multiple equal offers now. But the trap they share is singular.

The Year One Math and Why It Is So Seductive

Take the deck at face value for a moment. The displacement story, meaning Microsoft’s pitch to replace an existing third-party solution with one of its own, is real. Defender for Endpoint can replace CrowdStrike. Entra ID P2 can replace Okta. Purview can replace your data loss prevention (DLP), eDiscovery, and records-management stack. Intune can replace your MDM. Mimecast and Zscaler can be rolled into the Microsoft security envelope. The third-party invoices and multiple vendor tentacles go away. As alternate vendor contracts run out, displacement savings, at least on paper, can not only fund the upgrade but eventually may produce a net reduction. Multiply that by five years of declining-but-still-present discount and the spreadsheet is enticing.

It is designed to be. The math is the bait. The point of an MEO is to make the Year One comparison clean enough that procurement can defend the decision in a one-page memo to the C-Suite. The buzzwords do the rest. Nobody at the table wants to be the one responsible for everyone coughing in the wake of the competition’s AI dust cloud.

Here is an example of a table the account team will walk you through, missing the last two columns:

The whole proposal paints an ominous trajectory, and the last two columns are where the offers actually balloon. Both MEO paths look like deals in Year One (roughly E3 parity, by design) and both end the term materially above your current E3 ERP. By Year Five, the customer who took the E5 path is paying 58% more than their original E3, fully weaned off of any discount before the renewal even arrives. The customer who took the E7 path is paying 175% more, or almost three times the original E3 ERP, for a footprint they never evaluated on its merits, on a discount scheduled to vanish.

The technobabble is what stays. The deeper the Year One discount, the worse the Year Five reckoning. That is not a coincidence; it is the structure. And then the EA expires, and you renew, which is where the trap closes.

The Dependency Discount: The Contract Microsoft Is Actually Selling

While the bundle ramp is what you see, the dependency discount is what you buy. Each displacement under the MEO does two things at once. It eliminates a third-party vendor alternative, and it hardens a Microsoft-shaped dependency in its place.

Defender for Endpoint displaces CrowdStrike, and your Security Operations Center quietly retools its detection content, IR runbooks, and threat-hunting queries onto Microsoft’s stack. Entra ID P2 displaces Okta, and every SaaS integration in your tenant gets re-federated, and every Conditional Access policy gets reshaped around Microsoft Graph.

Every one of these displacements is defensible in isolation. If your team independently evaluated Defender against CrowdStrike on the merits and chose Defender, that is a legitimate decision. The MEO is not that decision. The MEO is six of those decisions wrapped in a single procurement signature, made simultaneously, on a five-year discount schedule, with no architectural review of the cumulative effect. It is an architectural Trojan horse, infiltrating one quarter at a time, paid for with a discount that erodes on a published schedule while the dependencies harden like curing cement.

It is worth being honest about merit. Defender has come a long way. Entra is fine for most organizations. But the MEO decision is not being made on any of these merits. The bundle is being chosen because it is cheap right now with eye-popping discounts applied, packaged as a single yes. Cheap right now, locked in later is a terrible basis for a decision that will outlast the EA term.

The Trap: The Renewal After This One

Now run the clock forward five years. The discount has eroded over the term to zero. Your renewal quote arrives at full Level A on E5 — or worse on E7. The Year One math that justified the MEO no longer exists. And the leverage you would normally use at this point, basically an assortment of best-of-breed alternative vendors, has been quietly removed during the term you just completed.

You are facing the highest price with the lowest leverage. That is not a coincidence. That is the product. The five-year discount was not a deal. It was the consideration Microsoft paid you to disarm your own negotiation at the renewal after this one. The MEO offers you multiple paths in. The outcome across all of them is singular, and it is not equivalent to anything you would have signed if you had seen it priced honestly.

And do not forget the tax applied to all of this: Unified Support, priced as a rolling 12-month look-back percentage computed against your new EA spend bar. Every dollar you add to the bar as the MEO discount erodes becomes a multiplier on a support contract that you cannot meaningfully decouple.

What Can a Customer Do?

The good news is that the MEO is defeatable, and not all of the moves require executive air cover or a full-blown architectural review board. Some of them just require doing work that procurement teams routinely skip. In rough order of how early in the cycle you should run them:

- Know your personas first

Most enterprises have not done a rigorous license-mix assessment of their actual user population in years, and the MEO works partly because that work always loses to other priorities. The account team is selling you a uniform bundle for all of your users because you can’t articulate why you shouldn’t buy one. If you actually segment your user base into categories like super users, knowledge workers, frontline workers, developers, contractors, you often discover certain combinations of subscriptions that will suffice for certain personas. The bundled MEO is wildly inefficient for that mix, and you cannot demonstrate that to your CFO without the user profiles work. Do this a year before you respond to the MEO, not after. Reconsider Google for your type of frontline workers as the “F3” plan necessitates tenant-wide security and compliance add-ons that catapult F-plans into the $22/month range.

- Reset the “business as usual” baseline before you compare anything

The MEO depends on the business-as-usual column being priced at full Level A so that the discounted alternatives look like deals. Refuse the premise. Demand that your waterfall discount or an equivalent discount off Level A, reflecting your actual volume and tenure, be reinstated on the Business As Usual (BAU) column. Then go further. Argue for renewal pricing that reflects a reasonable uptick over your exit price from the prior agreement, not retail. That is the honest comparison baseline.

This single move does not necessarily collapse the equivalency math. Microsoft can in principle pile enough discount on E5 and E7 to keep the columns aligned. But it forces the account team to decide whether they want to fund the discount levels required to keep the MEO game going against a more honestly priced baseline. Many won’t, because the deal-desk approval threshold for those discounts reaches upper limits, the MEO conversation pivots, and you can bring it back to your particular roadmap requirements. That is the outcome you want.

- For the CIO: Refuse the category

An MEO is not a pricing proposal. It is an architecture proposal with a procurement deadline stapled to it, and it should be evaluated by whoever in your organization actually owns architecture, including your architecture review board, your security architecture function, your enterprise architecture group, whatever it is called. Demand a multi-year total cost model that includes Year Five at full ERP, exit cost, and the cost to rebuild displaced capabilities if you ever need to. If your architecture function would not approve a five-year, six-vendor displacement plan on its merits in any other context, it should not approve it because procurement has a signature deadline.

- For procurement and software asset management: Decouple the displacements

Each displacement is its own decision, with its own business case, its own timeline, its own Proof of Concept, and its own contract. Do not let a bundle discount paper over numerous independent vendor evaluations. Stagger your third-party renewal dates so that at the next EA, at least some of those alternatives are live, contracted, and ready to scale and are not just theoretical. Model the exit cost from Microsoft alongside the entry price into Microsoft, because the cheapest deal at signing is the most expensive deal at the next renewal if you cannot credibly walk away.

- If you are signing anyway, negotiate the erosion rate and demand a Not-to-Exceed

Some MEOs will get signed regardless of what is in the prior four sections because procurement was overwhelmed, the persona work didn’t get done, the architecture function wasn’t asked in time, or, most commonly, leadership rests securely that “nobody got fired for buying the whole Microsoft stack” and the MEO is the path of least organizational resistance. If that is your situation, the conversation shifts from refocusing the requirements conversation to harm reduction, and there are still two contractual moves worth making.

First, negotiate the erosion rate. The 40 / 30 / 20 / 10 / 0 schedule (or its E7 equivalent) is a starting point computed on equivalency declining to zero over the term; it is a structure the account team proposed because it maximizes the trap. Argue for a flatter curve, which means a sustained discount across the term, ideally one that does not fully decay, or anchor on a flat discount for the full term, given some amount of determined value is indeed present.

Second, and more importantly, insist on a Not-to-Exceed (NTE) cap on the subsequent renewal, written into this contract. The NTE should contractually limit how much the per-user price can move at the renewal after the MEO term ends, capped at a small premium on the exit price and written very meticulously. This is the single contractual provision that directly addresses the thesis of this piece. It does not eliminate the dependency hardening, but it removes the pricing power that the MEO discount table was buying Microsoft.

If Microsoft refuses the NTE, that refusal is meaningful. Document it, escalate it to your executive sponsor, and use it. An account team unwilling to commit to bounded pricing at the next renewal is telling you what they intend to do at the next renewal, and you have just witnessed how that works.

The Discount Is Real; The Trap Is Real

The MEO is a playbook owned by Microsoft’s Sales Excellence organization, and it is being run on every enterprise renewal in FY27. The discount is real. The trap is real. Both are true at the same time, and a customer who only sees one of them is going to sign a deal whose true cost does not arrive until that next EA is on the horizon.

The work required by you is unglamorous: Persona analysis, baseline resets, architecture reviews, contract clauses. None of it is rhetorically satisfying. But all of it is the difference between signing a five-year discount and signing the disarmament of your next negotiation.

Don’t get defanged. A Directions on Microsoft advisor brings the persona analysis, the architectural lens, and the negotiation playbook to the conversation before the MEO does.