Microsoft’s Copilot 365’s Cowork feature, which is generally available worldwide as of June 16, will offer customers a choice of models and won’t be solely Anthropic-based as it is currently. Microsoft also is adding usage-based pricing to Cowork, on top of the Microsoft 365 Copilot license charges.

Microsoft made Copilot Cowork available to Frontier testing program customers in late March, 2026. Cowork, which allows customers to run complex, multi-tool tasks, supports Anthropic’s Opus 4.8 and Sonnet 4.6 today. For customers in the Frontier test program, there’s also an option to use OpenAI’s GPT 5.5. And “coming soon,” Microsoft plans to release an Azure-hosted model for Cowork that will “handle tasks at a substantially lower cost,” officials said. This Microsoft-developed model will be known as Cowork 1.

Microsoft CEO Satya Nadella spilled the beans on Microsoft’s plans to bring model choice to Cowork during an interview at Microsoft Build in early June. During that interview he said Cowork was a type of “form factor” for agents and it would be getting support for GPT in addition to Anthropic’s models. Nadella said the same way Microsoft 365 Copilot currently offers customers a choice of models, the same will be true of Cowork.

Copilot Cowork requires a paid Microsoft 365 Copilot user license, which retails for $30 USD per user per month. On top of that, Microsoft also will bill users for Cowork on a usage-based basis, with charges determined by the tasks they run. Users will be charged in Copilot Credits, with the price of each task calculated via four inputs: Model use, context retrieval, tool calls, and runtime.

There will be two payment options for Cowork: Pay As You Go (PAYG) and P3. P3 is for those who have a handle on cost projections and can commit to a usage volume in advance in exchange for a discount. Where multiple models are available, customers can use the model picker to manage cost-per-task, according to Microsoft.

Low Cost Provider

Microsoft’s strategy seemingly is to position its own models as the lower-cost option across its Copilot family as it evolves.

Microsoft is adding support for more models in its GitHub Copilot, as well. It is integrating its just-announced MAI-Code-1-Flash model to GitHub Copilot individual users and making it the default in the Auto picker there. (Currently, the default is OpenAI’s GPT 4.1.) Its plan is to continue to allow developers to select different models if they choose to do so. As of June 1, Microsoft is charging GitHub Copilot users on a usage basis.

Microsoft also is planning to release a Copilot “Super App” this summer, officials have said. That Super App will provide users with access to Copilot Chat, Copilot Cowork, Copilot Code, and Copilot Autopilots, which are agents that will run without user intervention (like its recently announced Scout personal agent, built on OpenClaw).

In related news, WorkIQ also is generally available as of today, June 16. And it also is adding consumption-based pricing to its model.

Work IQ is Microsoft’s “intelligence” layer built on top of the Microsoft Graph that mines customer data for Copilot. Starting June 16, the Work IQ API will require Copilot Credits and users will be charged directly when they build their own agents or apps calling the Work IQ APIs. They’ll also be billed if they use a third-party agent that uses Microsoft 365 data through the Work IQ APIs.

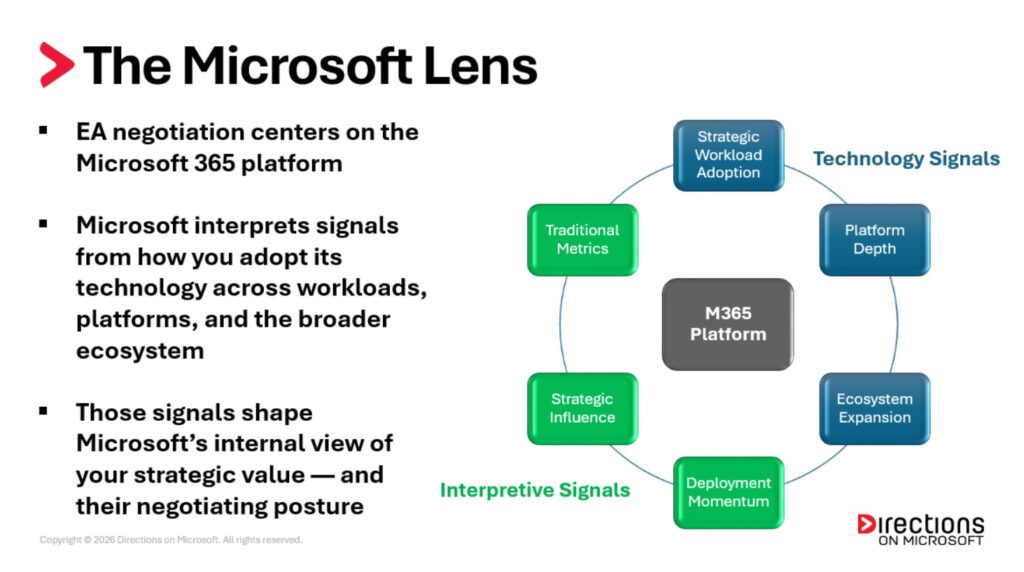

There is a question Microsoft Azure customers are only now beginning to ask. It comes after consumption data has been gathered, forecasts assembled, growth plans documented. A commitment figure sits on the table with a Microsoft offer attached. Then someone on the customer’s side asks about the capacity behind that number. If the customer commits its full spend and Microsoft cannot deliver the infrastructure to consume it, then what?

Silence.

Someone promises to take the question under advisement. The response is not evasion. It is unfamiliarity. Microsoft designed the Microsoft Azure Consumption Commitment (MACC) in a world where capacity was abundant, and forecasting consumption was an art customers were mastering. The capacity question never needed asking. But now that world is no more, and soon this will be the first question every customer asks.

Capacity Was the Answer. Now It Is the Question

On paper, the MACC is a simple bargain. You commit to consume a fixed dollar amount of Azure over a term, typically three to five years. Microsoft discounts the meter in exchange for revenue certainty. Microsoft created the model in an era of effectively unlimited cloud supply, when the only meaningful risk in the deal was the accuracy of your own forecast. Capacity was the unstated premise of the entire arrangement.

Now that premise is cracking. Microsoft’s own leadership has told investors, quarter after quarter, that demand for its cloud exceeds the supply it can provide. AI workloads are absorbing datacenter capacity faster than concrete can be poured, and chips can be racked.

The public evidence of strain is everywhere: Quota requests sitting in backlogs with no estimated fulfillment date, deployments struggling in flagship regions, customers redesigning architectures around regions they never intended to use. Customers are living it, and many have already paid for workarounds out of their own budgets.

Capacity isn’t only a pillar of the MACC. It was the founding answer of cloud computing itself, with the promise that cloud supply was more accessible and scalable than anything you could build yourself. The MACC simply converted that answer into a financial instrument. You could commit with confidence, because the cloud always has room.

Now scarcity is running that conversion in reverse. The MACC agreements under construction right now are still built for the old answer, not the new question.

No Actuary Would Approve This

Strip the MACC down to its economics, and it is an insurance contract, with the roles reversed from what you might expect. The customer underwrites Microsoft’s revenue certainty, and the discount is the premium Microsoft pays for that protection.

Viewed through that lens, customers are being asked to absorb dramatically more risk while collecting dramatically less premium. The structure asks you to forecast your consumption with precision at the very moment Microsoft cannot forecast its capacity with confidence. If capacity is unavailable, the financial obligation survives anyway; the commitment is owed whether or not the cloud shows up. Workarounds carry real costs, from standby architectures in alternate regions to engineering time spent routing around constraint, and none of it appears anywhere in the deal.

And displacement itself carries a price tag that Microsoft’s own published pricing quantifies with uncomfortable precision. A D16as v5 virtual machine that runs $68.80 per 100 hours in East US 2 runs $82.60 in South Central US. Same machine, same meter, 20 percent more. Across thousands of meters, the regions customers overflow into when flagship capacity runs out may carry premiums of 10 to 20 percent over the regions they leave, and some of the available alternates stock barely six of every ten meters that a flagship region sells. Your only choices may be to pay more, to re-architect, or to pay more and re-architect.

All the risk sits on your side, all the protection sits on Microsoft’s, and the committed dollars arrive in Redmond either way. No actuary would approve that policy, and no MACC proposal on a table today has this risk priced into it. The MACC negotiation has lawyers, architects, procurement, and IT in the room. It has never had an actuary, and that absence is about to become expensive.

The remedy is not a new hire. Most large companies already employ people who price risk for a living, in treasury, in insurance, in enterprise risk management. They have simply never been invited to this table. But in the era of scarcity, they belong there.

Risk professionals read price tags differently. To them, a number is not a price until the risk traveling with it is counted. Pay-as-you-go (PAYG) is the perfect example. PAYG has long been framed as the mark of an immature cloud customer, the thing from which a MACC uplevels you. But reweigh the equation with risk in it and the hierarchy inverts. List price is the only price on the menu that carries no commitment risk, as it gives you the freedom to redirect spend, to rebalance across regions or providers, to wait out a shortage without owing anyone for capacity that never arrived. Once risk is priced, retail can become the best price in the room. Customers running production workloads at scale without a commitment are not necessarily behind. Under the new economics, they may simply be early.

The Pause Is the Power Move

So is a MACC worth it at any discount? The honest answer is that nobody knows yet, including Microsoft. The economic principles underneath every commitment-style agreement have shifted, and the new equilibrium has not been found. The discounts have not adjusted to the risk. The contracts have not adjusted to the question. The institution selling the commitment has not yet absorbed how much the ground has moved beneath it. The answers are forming, on both sides of the table, in real time.

All of this means that if a MACC proposal is in front of you, or a commitment renewal is on your horizon, the most valuable move available right now costs nothing. Take a pause. A pause is not refusal, and not paralysis, but deliberate diligence in a moment when speed serves only the old playbook.

Before anything gets signed, certain questions deserve real answers. What happens, contractually, if you cannot consume because the capacity is not there? What is Microsoft actually committing in return, beyond a number on a meter? What is your pay-as-you-go position truly worth, both as leverage and as insurance? How should a commitment even be sized in a world where supply is as uncertain as demand?

Those questions deserve answers. This MACC blog series will work through them in turn: How to size a commitment against capacity nobody guarantees; what to demand from Microsoft in exchange for a MACC; when to decide paying retail is the smartest price on the table; how to understand the hidden geography tax built into Azure’s regional price map; how to price capacity risk before Microsoft prices it for you; and how to take into account that a supply-constrained vendor might quietly prefer that you not commit at all.

The MACC was built for a world of abundance, and that world is gone. Until the agreement catches up, treat every commitment proposal as what it has quietly become — an open question wearing the costume of a routine deal.

Azure MACConomics Series

Part 1: Is a MACC Worth It at Any Discount? (this article)

Build 2026 got me thinking, even more than usual, about Microsoft’s AI strategy.

Microsoft is not trying to win with the shiniest toys (although the Surface RTX Spark looks nice!). It’s working to position itself as the platform leader. Microsoft is building out an operating model, not a product portfolio. And it’s making a bet on the enterprise AI execution layer, not Copilot.

Why ROI Is the Wrong Lens

This bet may be surprising given the intense pressure Microsoft is under because Copilot adoption is lagging, CapEx expenditures are historically high and margins are under pressure, begging the question: How will Microsoft make money?

These questions reflect a short-term view, and Microsoft typically eschews short term gains for long term dominance. Windows, Office and Azure all followed the same pattern:

- Embed into the ecosystem

- Become default infrastructure

- Monetize at scale

Microsoft’s AI positioning is following the same playbook. Its approach is less about immediate profit and more about building platform lock-in that defines the enterprise for the foreseeable future. So, the lack of ROI at this point is simply a bump on the road towards its long-term strategy.

What Microsoft Is Actually Building

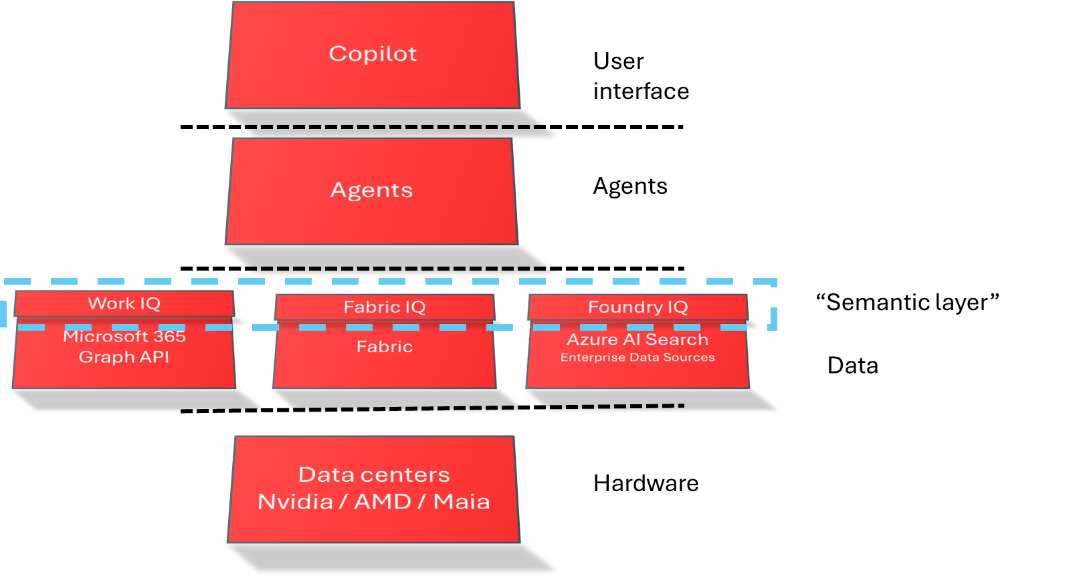

To understand the strategy, look at the system, not the products. At Build, Microsoft laid out a layered AI stack:

- Compute fabric: edge + cloud infrastructure

- Models: first‑party and partner models

- Context layer: enterprise data, semantics, knowledge graphs

- Runtime: agents executing workflows

- Control plane: identity, governance, security

This architecture was described in the keynote as a cohesive stack — from “compute fabric” to “security, compliance, and governance.” The key insight is that these capabilities are converging into a coordinated system. Microsoft is endeavoring to define how AI work is executed, not just enabling it.

From Partnership to Control

There is also a shift happening under the platform. Microsoft’s initial AI strategy relied heavily on OpenAI. Although that relationship remains important, it’s changing. And its evolving positioning is not about Anthropic.

At Build, Microsoft showcased seven of its own models and chips, emphasizing that they rivaled their partners on performance and costs. It also debuted new hardware with NVIDIA and Qualcomm, trying to capture the developer and frontline worker experience end-to-end.

This repeats Microsoft’s pattern of using partnerships to accelerate entry into the market, internalize critical layers and consolidate control over the platform. OpenAI and Anthropic remain critical partners of Microsoft, but Microsoft is moving to reduce dependency on them and step towards controlling the execution environment.

Where Lock‑In Actually Happens

Many enterprises think of vendor lock-in in terms of models and APIs. Microsoft’s strategy changes that view by focusing on lock-in on data, identity, governance and workflow.

Microsoft is building a “context layer” as a first‑class platform component with Microsoft IQ, and specifically the Fabric and Foundry knowledge bases. This defines how enterprise knowledge is structured and accessed for agentic use and extends dependencies beyond traditional storage and databases.

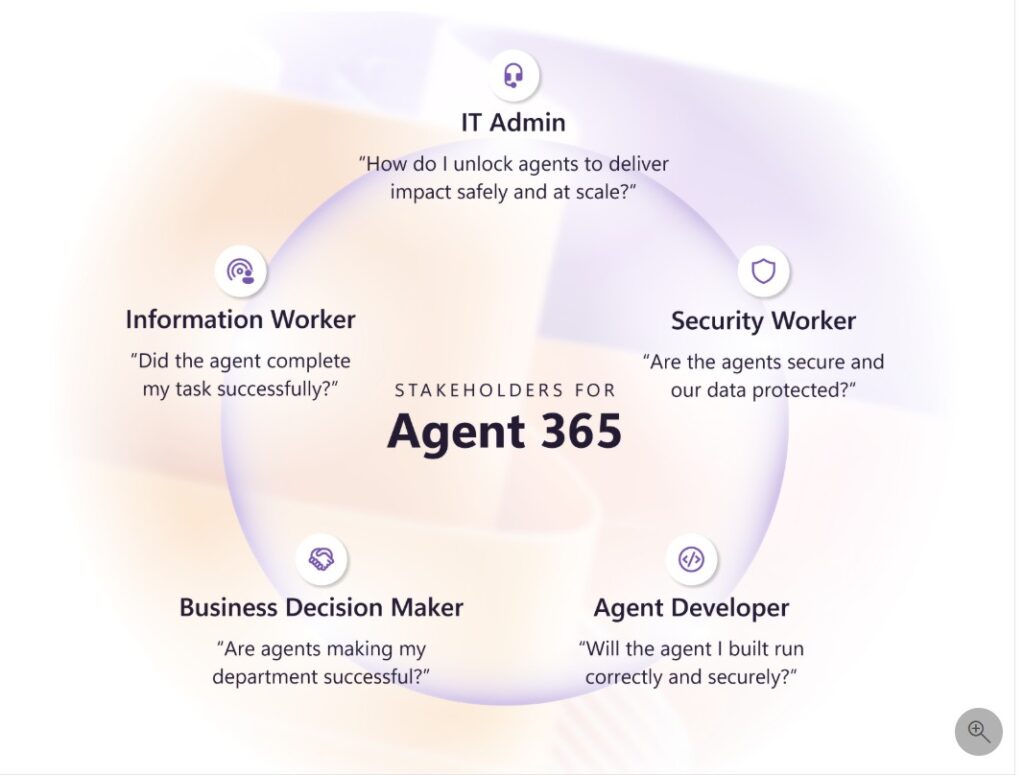

Agents are being treated as first-class identities, “requir(ing) their own identities, access controls… even when they’re working on your behalf.” Once agents are provisioned as identities inside Entra (Entra Agent ID), Microsoft controls who or what can act across your enterprise.

Governance is embedded into the execution layer of agents with Agent 365, Defender and Purview. “(E)very agent…needs to be managed with the same rigor as users, apps, and devices,” according to Microsoft. The potential scale of agents requires platform enforcement and can’t be done by policy alone.

AI is already being embedded where work happens. Once AI is embedded in Teams and Office workflows, switching platforms is a change in how work gets done across the organization.

As the keynote emphasized, agents rely on continuous loops of “storing, retrieving, reasoning, acting, and learning” against enterprise data. Once those loops are embedded into your systems, switching vendors is an operational exercise, not just a technical one.

A New Financial Model: Consumption Over Licenses

AI also shifts how software is paid for. Software is typically a predictable license cost, but AI is turning that concept on its head as it increasingly is based on variable consumption (tokens, compute, agent activity). Microsoft has made this explicit with its focus on optimization metrics like “tokens per dollar per watt”.

This change introduces a new set of risks with AI. Consumption based pricing is inherently volatile with little means to predict costs, making budgeting difficult. AI becomes more like cloud compute but potentially a higher order of magnitude because of autonomous agents. This is significant shift in cost management.

The role of M365 Copilot is perhaps the most misunderstood piece of the puzzle. Microsoft is constantly criticized for Copilot’s lack of adoption. However, what matters is not Copilot’s adoption as a standalone product per se, but it’s becoming the universal interface where work gets done — coordinating agents, accessing enterprise context and executing workflows. This aligns with what Microsoft described as moving from chat to “multi‑step tasks” and eventually to autonomous “autopilots” running in the enterprise.

The Real Executive Decision

Microsoft is raising the stakes on enterprises who are deciding on an AI stack by embedding its operating model, which pits a “better together” approach against “best of breed.” Customers’ decisions on their vendor of choice can have implications for years to come.

Choosing Microsoft’s AI platform (and its better together promise) could result in faster deployments, integrated governance and reduced integration hassles but at the cost of reduced flexibility and long-term dependency on Microsoft. This option may appeal to enterprises who benefit from using AI but not building AI.

Otherwise, enterprises can create their own AI stack with multiple vendors (best of breed). This gives them greater control over architecture and optimization but can lead to integration complexities, uneven governance, and reduced time to value. This choice may be appealing to enterprises whose business model depends on building AI tools and systems instead of just using them.

What to Watch Next

Microsoft is trying to define the default enterprise AI platform. Look for continued shifts toward first party control (Microsoft models), enterprise control planes (Agent 365 and Foundry Control Plane), more consumption-based and agent-as-user pricing and the strategic role of Copilot and the coming Copilot “super app.”

The companies that benefit most from AI will not be those with access to the best models. They will be those that make an explicit, well understood decision about who controls their platform and the long‑term consequences of that choice.

Last year’s Microsoft Build developer conference focused heavily on agents. But this year’s Build, which kicked off June 2, is almost entirely agent-focused.

Microsoft is working to position everything from the Windows OS itself to coming high-end Windows PCs and single-purpose agent devices built on Android as custom-built to enhance customers’ agent experiences and developers’ ability to build them.

Microsoft has been trying — and largely failing — to get customers excited about running AI locally, even though doing so could help cut cloud computing costs. (CEO Satya Nadella said the appeal of this local approach is that it brings “unmetered intelligence” to users.)

Windows Client Improvements In The Pipe

Microsoft’s attempt to make Recall, its searchable visual timeline feature, a reason to buy so-called “Copilot+” PCs stalled after experts warned Recall was a security risk. Microsoft ended up backing away from its Copilot+ PC branding campaign in late 2024 but continued to try to push Foundry Local (the rebranded Copilot runtime) as a compelling capability for developers.

At Build, Microsoft’s updated pitch is that Windows is the best platform for building agents, and not just agents for Windows.

It’s not about “Windows for ‘Windows developers,’” Microsoft says in its Build blog post. It’s “Windows for developers, period.”

Microsoft showed off at Build a new sandboxed agent runtime, new shell and terminal experience, new Windows Subsystem for Linux containers, and other Windows features it is counting on to attract agent/AI developers. Coreutils for Windows, which is a set of Linux-like command line utilities that run natively on Windows is now generally available, as well.

New High-End ARM-Based Windows PCs and New Dev Box On Tap

Just ahead of Build — at Computex on May 31 — Microsoft and Nvidia made announcements around Nvidia’s coming RTX Spark chip, which will power a new wave of high-end Windows PCs from Microsoft, ASUS, Dell, HP, Lenovo and MSI starting this fall. RTX Spark is an ARM-based integrated chip targeted at the same market that Apple targets with their Pro and Max Apple Silicon chip, although Nvidia also took pains to emphasize RTX Spark’s gaming credentials.

Microsoft showed off an early version of the coming Surface Laptop Ultra, its MacBook Pro competitor built on RTX Spark that is due this fall but provided no pricing and no full spec list. At Build, officials also announced there also will be a Surface RTX Spark Dev Box, designed for sustained workloads, long-running training, and agentic AI jobs, available later this year in the U.S. (orderable via Microsoft.com/devbox for some as-yet-unknown price).

While users can already run agents locally on certain Windows PCs, Microsoft is positioning the coming RTX Spark PCs as providing a more secure Windows platform for on-device agents. Details as to how these enhancements will show up in Windows 11 are vague, but Microsoft is promising to add new “Windows primitives” that will provide built-in identity, isolation and governance capabilities designed to make developing, testing, and running agents locally on Windows devices a better and safer task.

Android-Based Agent-First Devices; Private Pilot Coming Up

During the June 2 Build keynote, Microsoft also showed off some proof-of-concept enterprise-focused devices that it is developing as part of its “Project Solara” agent-first device platform. Microsoft is working with silicon partners on Android Open Source Project (AOSP)-based devices that could be tailored for healthcare, retail and financial customers.

Officials showed off a wearable badge concept device that could be used by information workers, frontline workers, nurses or anyone needing secure access to a space. The badge could provide users with a glanceable Priority Agent or the existing Microsoft Facilitator agent to record a hallway conversation. Microsoft also showed off a “desk concept” device (that’s similar to a standalone speaker) that would allow users to access their PCs/monitors and Windows 365 clients via voice.

Microsoft is planning a private pilot of the agent-first devices with AccuWeather, Best Buy, CVS, Levi’s, and Target “in the coming months,” officials said. And it is planning to work with silicon partners including MediaTek, Qualcomm, and others, on building a range of devices, officials said.

Clawing Ahead With OpenClaw

At Build, Microsoft took the wraps off the software development kit for the Microsoft Execution Containers (MXC) agent-native runtime, which is now in preview. MXC will give developers and admins an enterprise-grade sandboxed environment for agents, enforced by Windows everywhere that agents run.

Agent 365 native integration with MXC — which Microsoft says will bring Defender, Entra, Intune and Purview protections — to secure local agents and reduce risk, will be in preview in July. The MXC technology is now being used by OpenClaw on Windows, and Nvidia’s OpenShell runtime for Windows will be built on MXC, and includes policy management, inference routing and other features for agent developers.

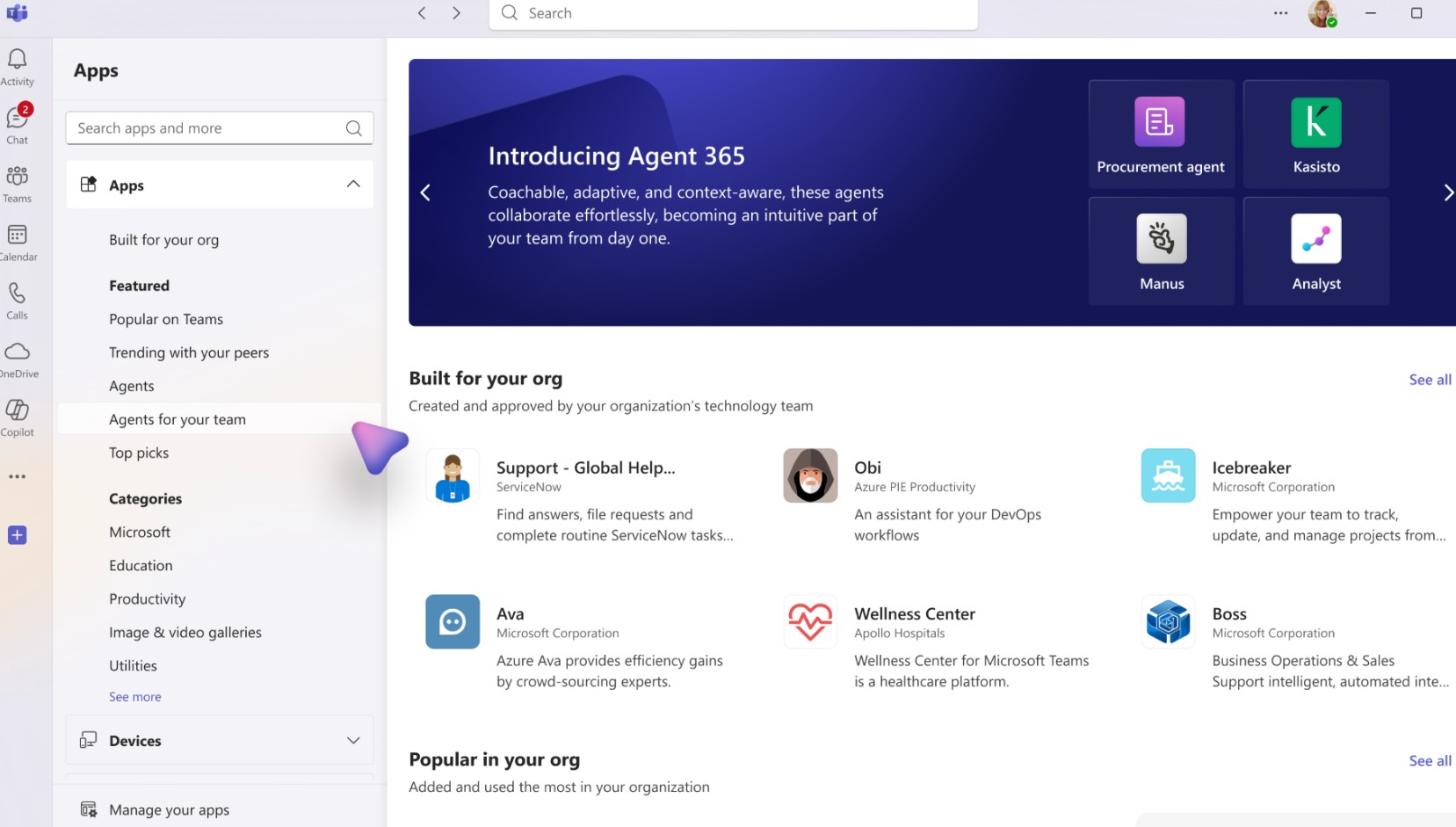

On the topic of OpenClaw, Microsoft also is moving ahead with productizing an OpenClaw-based skunkworks project that has been in the works for a couple of months under the name “Microsoft Scout.” Scout, a personal assistant, meant to work across work data in Teams, SharePoint, OneDrive and more, with built-in enterprise-grade security controls. Scout has been in testing inside Microsoft since May; Microsoft now is opening a preview to those in the Frontier experimental channel.

Microsoft officials said Scout is the first of a category of agents it’s calling “Autopilots.” Autopilots are always-on agents that can work autonomously and have their own identities, so they can act on users’ behalf in the background, without needing to be prompted each time.

Microsoft also announced some new and updated Microsoft-built AI models, including its first reasoning model, known as MAI-Thinking-1, which Microsoft claims will come at a low-token cost. Officials said it was built “from the ground up on clean data, without distillation from third-party frontier models.” It’s available now to “select early partners.” And it unveiled a new GitHub Copilot desktop app (in preview), which it is pushing as being perfect for agentic development.

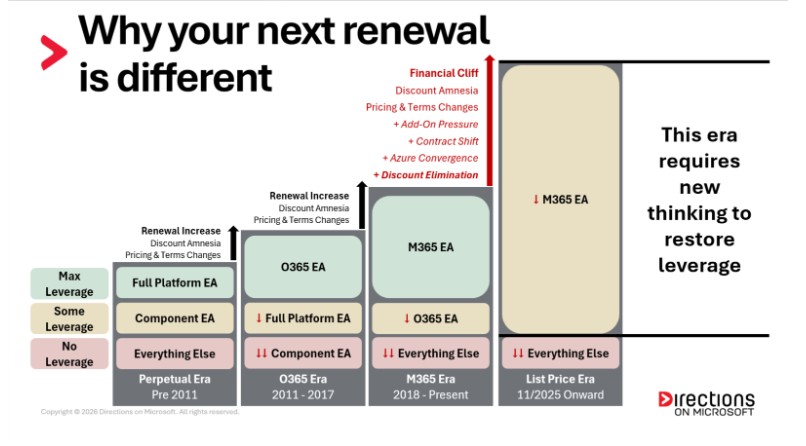

Unified Support has always been its own source of frustration: Expensive, opaque, and widely regarded as the one Microsoft line item that feels least like a choice. What has changed is the context. The November 2025 pricing changes that created the Financial Cliff also created something most customers have not yet calculated, namely a Unified Support cliff. Every dollar of price increase that flows through your Enterprise Agreement (EA) base flows through your Unified Support calculation as well. The EA cliff is visible. The Unified cliff is hidden and compounding.

How Microsoft Changed the Unified Game

Microsoft’s November 2025 pricing changes have been analyzed extensively in terms of their direct EA impact. What has received less attention is the downstream effect on Unified Support.

The Unified Support fee is calculated against your Appraised Product Spend, which is a baseline derived from your actual Microsoft purchases over the preceding period. When your licensing costs increase, that baseline will eventually increase. Your Unified fee recalculates against the higher number. The support tax inflates even if your consumption is flat, even if your headcount is unchanged, even if the only thing that moves is Microsoft’s price list.

This dynamic is not new. What is new is its magnitude. The November changes represent the largest structural repricing of the Microsoft commercial stack in years. For organizations whose Unified renewal is approaching, the compound effect of higher licensing costs flowing into a percentage-based support calculation deserves its own line in the financial model.

A second pressure is building alongside the pricing changes. The era of abundant, competitively priced cloud infrastructure is giving way to an environment of capacity constraint. Azure costs are no longer declining as a function of competitive pressure and scale economics. They are, in some categories, moving in the other direction. For organizations with significant Azure commitments, this means the Appraised Product Spend baseline is under pressure from two directions simultaneously — Microsoft’s pricing decisions and market-driven cost inflation. Both flow through to the Unified calculation.

The program itself has also changed. Microsoft’s Unified Support Services Description, the document that defines what the program actually covers and is incorporated by reference into every Unified agreement, was updated twice in the second half of 2025 and again in May 2026. The scope of included services has been quietly refined. The premium tier structure has expanded. The terms governing what customers receive for the base fee are not the same terms that governed agreements signed two or three years ago. Customers who have not reviewed the current document against the one in force at their last renewal are making decisions based on an incomplete picture.

Three New Pages for Your Playbook

Unified Support has never been a passive line item. Customers have negotiated it, debated it, and in many cases constructed sophisticated strategies for managing it. The playbook those strategies produced was not wrong. It was rational, built on a reasonable understanding of how the program worked and what alternatives existed.

What has changed is the underlying conditions that made the playbook rational. Here’s what you can do right now to make your approach more effective:

Maintain a living Unified support strategy. The conditions governing your support economics now change between renewal cycles, not just at them. Program terms shift. The alternative market moves. Your own spend profile evolves in ways that change where you sit in the rate structure. A strategy built once and revisited only at renewal is already behind the curve. The customers who are winning these negotiations are the ones who treat Unified support as an ongoing posture, not a periodic decision.

Negotiate your Unified agreement as part of your integrated Microsoft strategy. The base fee is progressive and calculated as a percentage of your Microsoft product spend, which means your EA and Azure commitment decisions have a direct downstream effect on your support cost. The form of any Microsoft investment in your renewal matters too. A consumption discount reduces the spend base your Unified fee is calculated against; a project funding commitment does not. Customers who bring all of these levers into a single negotiating conversation consistently extract better outcomes than those who sequence them separately.

Evaluate third-party support options as a formal part of your next renewal. The alternatives to Microsoft Unified Support have matured to the point where a credible market exists, and new models are showing early green shoots. What was once a binary choice between staying with Microsoft or taking a leap into the unknown is now a genuine spectrum of options at varying stages of market maturity. Getting the best possible outcome, whether that ultimately means staying with Microsoft, augmenting your agreement, or moving in a different direction entirely, begins with a rigorous evaluation of what that spectrum actually looks like today. This is not a theoretical exercise or a negotiating bluff. It is how you build leverage regardless of where you ultimately land.

New Players Are Also Changing the Game

The Unified Support conversation has always had more options than the conventional wisdom suggested. CSP partners, independent third-party providers, and hybrid arrangements have existed for years. What has changed is the maturity of those options, and the market conditions that make evaluating them not just reasonable but necessary.

While pay-per-incident support exists as an option for organizations with minimal support needs, the customers this blog-post series addresses require something more structured. The question is not whether to have a support strategy, it is which one to adopt. You now have a genuine spectrum, and choosing among them intelligently requires understanding what each one actually delivers today, not what it delivered three years ago. A customer who has genuinely considered that spectrum negotiates from a stronger position. Your options include:

Stay with Microsoft and Negotiate on New Terms. This remains a viable path, but the negotiation has new dimensions. Microsoft’s Unified Support pricing contains more flexibility than the program’s structure implies, and the existence of credible alternatives has created leverage that did not exist five years ago. Customers who approach the negotiation with a clear understanding of how the fee is calculated, what has changed in the program terms, and what the market actually offers are consistently extracting better outcomes. The information advantage is real, and it is available to anyone willing to build it.

The Hybrid Model: Keep Some, Replace Some. An emerging category of enterprise buyers is choosing to retain Unified Support for strategic cloud workloads while engaging independent third-party providers for mature, stable technologies where Microsoft’s cost premium is hardest to justify. This model preserves the Microsoft relationship for the services where it matters most while creating significant cost reduction on the portion of the estate where alternatives are fully capable. This approach is gaining traction among large enterprises with mixed environments and is now supported by a growing ecosystem of qualified providers.

The CSP Model: Support Built Into the Partner Relationship. For organizations whose Microsoft relationship is migrating toward the Cloud Solution Provider (CSP) model, support is not necessarily a separate procurement. CSP partners with meaningful Microsoft relationships can provide first-line support backed by Microsoft’s escalation infrastructure, effectively bundling support into the broader partner relationship. This is a different architecture than traditional Unified Support, with its own trade-offs, but it represents a genuine alternative that did not exist in its current form at the last major renewal cycle for many enterprise customers. One important nuance is that the CSP market is itself competitive, and both support capabilities and the range of add-on options vary considerably from one partner to the next. The partner already in your ecosystem is a starting point, not a default.

Pure Third-Party Replacement. This path has been documented extensively and the market for it has matured considerably. Independent providers have demonstrated the ability to handle enterprise-scale Microsoft support at a fraction of the Unified cost for the right customer profile. The quality of providers varies, and the evaluation process matters. What was speculative several years ago is now a legitimate, recognized category.

An Emerging Concierge Model. A nascent but logical extension of the hybrid concept may be beginning to surface: organizations that keep their Unified Support agreement intact but engage a third party to own the operational mechanics of managing it. The administrative burden of Unified Support is real, and there are early indications that the market is beginning to respond to demand for that burden to be absorbed by specialists. This model is early stage. At least one organization is known to be experimenting with it. Whether it matures into a mainstream category remains to be seen, but the conditions that would make it viable now exist.

Plays the Game Is Still Working Out

The plays outlined in this section are not yet standard moves at the renewal table. They are observations that sophisticated buyers are beginning to make, worth adding to your playbook now, while they still represent an advantage.

Know Where You Sit in the Rate Structure and Question How You Got There. Episode 4 of this series examined Modern Work workloads that surface as Azure meters: Purview, Entra, and others that are functionally M365 but billed as cloud consumption. The Unified Support rate structure adds another layer to that conversation. Modern Work spend and Azure spend follow different rate curves, and where a given workload lands within that structure has real financial consequences. If certain Modern Work workloads are being calculated against Azure rates rather than Modern Work rates, the direction of that impact depends entirely on where your total spend falls.

At lower spend levels, Azure rates run higher, a potential cost penalty. At higher spend levels, those same Azure rates eventually drop below their Modern Work equivalent, a potential advantage. The question worth asking is not just what you are spending, but how that spend is being categorized and whether that question has ever been examined carefully. The rate structure is knowable. How your specific workloads map against it may deserve a harder look than it has received.

The Form of Microsoft’s Investment Is Gaining New Importance. Not all Microsoft concessions reduce your Unified Support base. An Azure consumption discount reduces your Appraised Product Spend directly, which flows through to a lower Unified Support baseline. An End Customer Investment Funds (ECIF) commitment funds a specific project but does not touch the Unified calculation at all. When Microsoft’s investment in a renewal takes multiple forms, the real question is less about choosing one over the other and more about how to weight them deliberately. A mission-critical project may well be worth prioritizing over a marginal reduction in your support base. But that should be a conscious trade-off, not an invisible one.

With Microsoft’s pricing increases driving up the Unified Support baseline, the downstream consequences of how a concession is structured are now more meaningful than they have ever been. This is also why negotiating holistically matters: the more agreements you bring to the table simultaneously, the more flexibility you have to shape that balance in a way that optimizes across your total cost of ownership, not just one line item.

Your Unified Fee Is Calculated on Yesterday’s Spend. That Window Is Closing. Many customers currently find their Unified fee calculated against a spend baseline that predates the November 2025 pricing increases, a temporary reprieve that will close at their next recalculation. When it does, the increases flow through in full unless offset by something negotiated in the interim. Discounts negotiated into your EA and Microsoft Azure Consumption Commitment (MACC) today reduce the effective spend your next Unified calculation will be based on. The better the negotiation now, the smaller the blast radius when that recalculation arrives. The lag, in other words, is not just a limitation. It is a planning window. The question is whether you use it.

Your Move

The short-term imperative is straightforward. Update your playbook. Align your Unified negotiation with your EA and MACC wherever the timing allows. And engage the full spectrum of Unified alternatives with genuine intent, meaning real quotes, real conversations, real comparisons across the options. Whether you stay with Microsoft or move in a different direction, the intelligence that process produces is the foundation of a credible negotiating position. These three steps will produce better outcomes at your next renewal regardless of which path you ultimately choose.

The long-term imperative is less visible but equally important. The observations outlined above are not yet standard renewal conversation. They are the leading edge of a more sophisticated understanding of how Unified Support economics actually work and how they interact with your broader Microsoft commercial relationship. The customers who build that analytical muscle now will be the ones setting the terms of the conversation when these dynamics become mainstream.

The old playbook was built for a Microsoft that operated with relative commercial stability and an abundance of resources. The pricing structure was predictable. The program was what it said it was. The alternatives were limited. None of those conditions hold in the same way today.

The November 2025 changes did not just raise the price of your Microsoft licenses. They accelerated the obsolescence of an approach to Unified Support that was already showing its age. The customers who recognize that will build something better. The ones who don’t will keep running a strategy designed for conditions that no longer exist, and the gap between those two groups will widen with every renewal cycle.

Your Next EA Renewal Series

Part 1: How to Avoid the Financial Cliff

Part 2: Why the Microsoft Lens Matters

Part 3: Why Your M365 Roadmap Is the Key to Negotiation

Part 4: A Multidimensional Agreement Demands a New Strategy

Part 5: What’s Hiding in Your Azure Bill?

Part 6: Your Unified Support Playbook is Overdue for an Update (this article)

Microsoft no longer wants midsize enterprises on the Enterprise Agreement (EA). The de facto floor for an EA renewal has been creeping upward for years, and customers in the 2,500-to-10,000 user band. Microsoft has decided this group is too small to command the direct account management it reserves for its largest accounts and too operationally complex to fit a SaaS-only playbook. Microsoft is steering these customers toward the Microsoft Customer Agreement (MCA) purchased through a Cloud Solution Provider (CSP). For these customers, the move is not optional. An EA renewal may not be an option any longer and there’s likely no rep to whom to talk. (How far up-market this push extends in Microsoft FY27 is the next question.)

Many CSPs are doing their best to accommodate these EA transitions. However, Microsoft is guiding these customers into a channel it has not equipped to properly handle these migrations. There is no formal certification program for CSPs taking on EA migration work, no required training curriculum, no qualification standard, and no SKU parity between what’s available in the channel customers are leaving and the channel they are entering.

Clearly, Microsoft is trying to pull Software Assurance off life-support, but the CSP subscription alternatives are financially untenable. The institutional knowledge that the legacy Large Account Reseller (LAR) channel accumulated over 20-plus years of EA work doesn’t carry over into the latest pureplay CSP newcomers, and Microsoft has shown no urgency to close either the knowledge gap or the program gap with appropriate transition SKU tooling.

What Microsoft Built, and What It Didn’t

The MCA-through-CSP channel was designed for cloud-first customers buying SaaS subscriptions. For that population, it works adequately. For midsize enterprises with mixed estates — factory floor terminals running Windows by device, retail point-of-sale kiosks licensed for Microsoft 365 Apps per device and Office Standard LTSC licensing, Windows file and print servers covered by Software Assurance (SA), on-premises SQL Server with SA-enabled new version rights, Remote Desktop Services device CALs and the like — the channel has structural gaps that midsize customers will discover only after they sign.

Most CSPs cannot transact Software Assurance without side partnerships with resellers that sell Open Value or Microsoft Products and Services Agreement (MPSA)-type arrangements where SA and perpetual license-only purchases are still buying options. Per-device Microsoft 365 Apps for Enterprise, a SKU that legitimately exists for shared-device populations under the EA, does not exist in the CSP price list. From-SA pricing and step-up SKUs, both of which most midsize EA customers rely on, have no CSP equivalent. There is no annual true-up to reconcile usage uptick, and the order return window is five days.

These are not edge cases. They are the daily operational reality of the customers Microsoft is pushing into the channel.

In other partner ecosystems, such as Azure Expert Managed Service Provider (MSP), the Solutions Partner program, the AI Cloud Partner, Microsoft invests in partner enablement, technical certification, and ongoing assessment. For EA-to-CSP migration, there is no equivalent license knowledge certification. The work is being done, and the customers are being signed, but Microsoft has built no apparatus to ensure the quotes are accurate and compliant.

What This Looks Like in Practice

A recent advisory engagement involving a multinational client with thousands of users illustrates the consequences. The customer’s expiring EA was actually an EA-Subscription (EA-S), a less common cousin to the EA where even SA line items are purchased as ‘leased’ licenses, so no underlying perpetual licenses exist. Multiple quotes received by the customer from global systems integrators marketing themselves as EA-to-CSP specialists revealed two distinct flavors of compliance exposure, each traceable to a structural gap Microsoft has not closed.

In one approach, a CSP proposed continuing the customer’s SA line items through an Open Value agreement layered alongside the new CSP subscriptions, at a cost of roughly $982,000 in annual SA. But the proposal was non-compliant. EA-S is a rental construct in which no perpetual base licenses are ever acquired, so SA-only continuation is not a viable option. There were no base licenses to attach SA to, and Open Value could not manufacture them retroactively. Five material Teams line items were also omitted entirely, as if inconvenient or unavailable.

Had the customer signed, they would have paid nearly a million dollars for a benefit they could not legally exercise and would have entered the new term carrying a missing license component that a future Microsoft audit would value at approximately $3.9 million to cure.

In a second approach, a CSP regurgitated the customer’s existing EA-S bill of materials verbatim, attached CSP prices, and called it a quote. Among the line items was Microsoft 365 Apps for Enterprise By Device, which was the part name the customer had been using under their EA-S for shared worker kiosks. However, that SKU does not exist in the CSP price list even though it was parroted back on the quote. CSP allows Microsoft 365 Apps for Enterprise on a per-user basis only. Because the customer’s user population was roughly three times their kiosk device count, a per-user purchase sized to the device count would have left them short by thousands of user licenses, with an annual licensing shortfall exceeding $2.6 million once user provisioning outran the licenses ordered by device. The CSP return window is five days. After that, the order is final.

A third quote, from a legacy LAR-CSP, caught both issues, identified that SA could not be carried forward from an EA-S, flagged that per-device Microsoft 365 Apps for Enterprise has no CSP equivalent, and proposed a compliant, if more expensive, alternative structure. The LAR caught what the CSPs missed because the LAR channel still carries the institutional knowledge.

Unfortunately, LARs with this kind of expertise are becoming harder to find. Microsoft has systematically reduced LAR margins and incentives over the past several years, accelerating consolidation in a channel it once invested heavily in building. The knowledge exists, but the organizations that carry it are fewer in number and harder to access than they were a decade ago.

Your Four-Point Compliance Checklist

If your organization is in the midsize band and approaching an EA renewal that Microsoft will not offer, run the following checklist against every CSP quote you receive. A CSP that cannot answer all four in writing is not equipped to migrate your agreement.

On-premises servers and CALs. Inventory your Windows Server, SQL Server, Exchange Server, SharePoint Server, and Remote Desktop Services (RDS) deployments still running on-premises, and identify which are covered by SA. Pureplay CSPs cannot typically transact SA in-house. If you have a meaningful on-premises footprint, your CSP must partner with a LAR or you will need a parallel MPSA or Open Value Subscription. Keeping servers on a standalone Server and Cloud Enrollment (SCE) is also an option (often, not a great one). The quote should identify this explicitly.

Per-device licensing for shared workstations. Identify factory floor terminals, retail point-of-sale kiosks, call center hot-desks, or any other shared device population currently licensed by device. CSP offers Microsoft 365 Apps for Enterprise per user only. Confirm in writing how your CSP intends to handle this and what the cost differential looks like under per-user assumptions.

From-SA pricing and step-ups in your current EA. Review your EA Customer Price Sheet (CPS) and identify every line item priced with From-SA discounts or acquired via step-up. None of these constructs exist in CSP. Your CSP quote should explicitly identify replacement SKUs and acknowledge the price delta.

True-up posture and license position confidence. Assess how confident you are in your current license position. CSP has no annual true-up. There is no structured opportunity to clean up usage drift, and the order return window is five days. Your Software Asset Management (SAM) processes for license reconciliation and reporting must adapt. For midsize enterprises with on-premises sprawl, license position uncertainty is the default — commission a third-party software asset management review before you sign to consolidate, optimize and cross-check, not after.

What to Do Before You Sign

Treat the migration quote itself as a checklist .Ask every CSP candidate to respond to the four items listed above in writing, line by line, before any commercial discussion. A CSP that cannot answer them in detail is not equipped to migrate your agreement.

Remember: The audit exposure, the operational disruption, and the cost of curing problems introduced by the reseller all fall on you, not Microsoft and not the CSP. The onus has always been on the customer and the agreement says so explicitly.

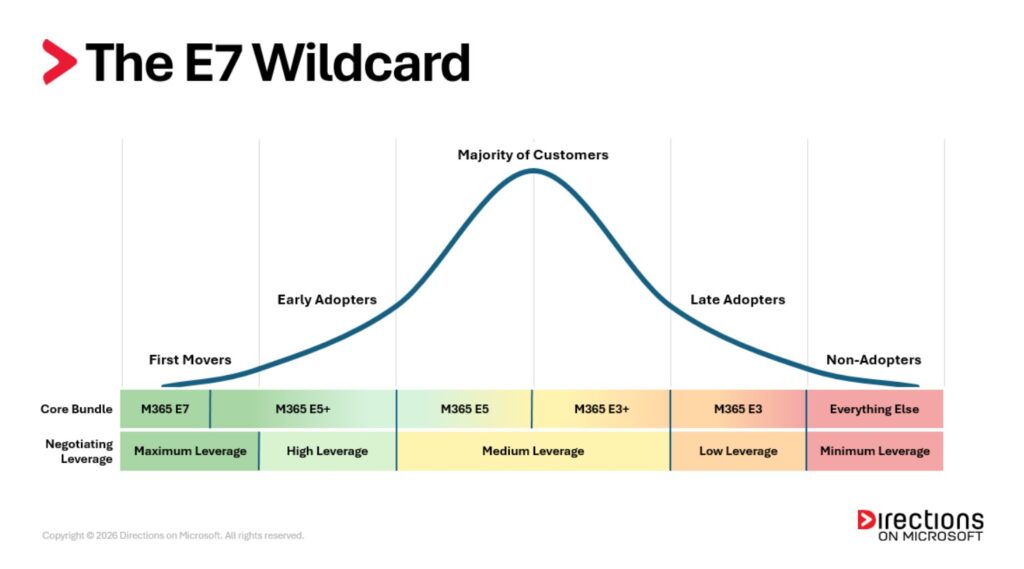

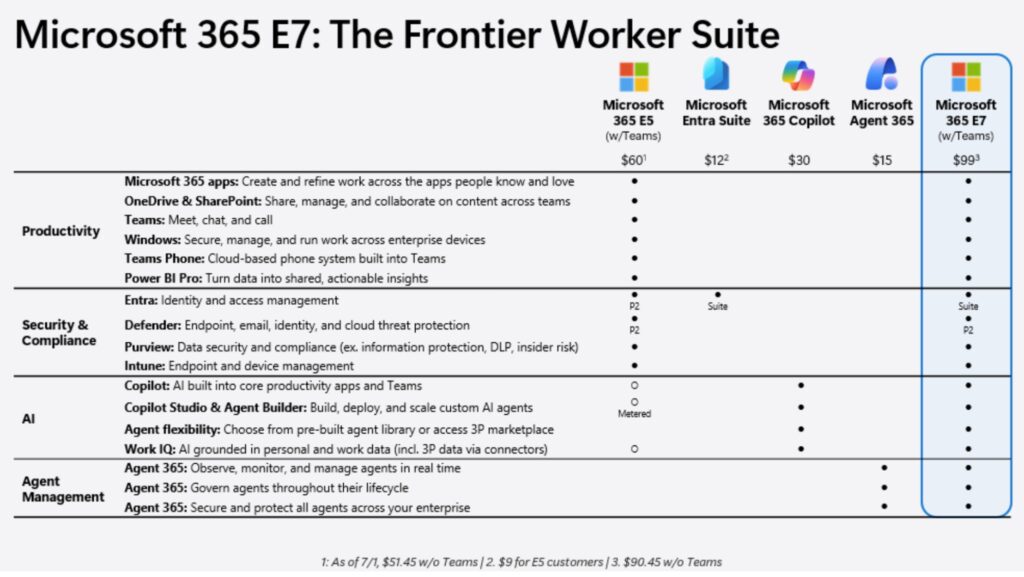

Microsoft rarely releases a new enterprise suite. M365 E5 arrived almost a decade ago, and nothing of comparable significance has followed until now.

M365 E7 is not an incremental upgrade. It is a platform bet on AI at the exact moment AI is rewriting enterprise technology in ways for which no multi-year agreement can fully account. That combination makes whether or not to go M365 E7 the most consequential Microsoft licensing decision in a decade. Microsoft knows it. Their field teams have been briefed, their sales motion is running at full speed, and their fiscal year closes June 30. They are not calling timeout.

The Play: Turning AI FOMO into a Hasty Step-Up Decision

Microsoft’s approach to M365 E7 adoption is not subtle. Field teams are going directly to the C-suite with an AI vision story, bypassing the IT and procurement teams who would normally conduct the due diligence. The message seems compelling: AI is transforming every industry, reshaping workforces, and redefining what competitive advantage looks like. M365 E7 is Microsoft’s answer.

The C-suite gambit has been part of Microsoft’s playbook for decades. What makes this moment different is AI FOMO. Fear of Missing Out, or FOMO, is real in the AI era. The concern that competitors are moving faster, that the automation wave will leave your organization behind, that hesitation today means falling behind tomorrow. Microsoft is capitalizing on that anxiety deliberately, and they are very good at it.

C-suite leaders are scrambling to understand and employ AI to their competitive advantage. Microsoft arrives with a bold story that sounds good, and they may not be wrong. M365 E7 could well be part of the answer.

But Microsoft does not arrive with a comprehensive agreement framework. They arrive with a step-up amendment and a signing deadline. A decision that deserves months of preparation gets compressed into weeks. And the negotiation that deserves the full weight of a major commercial event gets treated as a routine administrative action.

Why a Step-Up Is an Unbalanced Full Negotiation

This is the part that matters most and gets the least attention.

A properly negotiated M365 E7 renewal is a major commercial event. It involves usage analysis, structural term negotiation, competitive scenario modeling, multiple rounds of offers, and independent validation of whether the economics actually work for your organization. Customers who go through that process understand what they are committing to and why.

A step-up feels like a minor administrative action. You are upgrading a tier on your existing Enterprise Agreement (EA). The paperwork is lighter, the timeline is shorter, and the urgency is Microsoft’s. The decision feels smaller than it is.

But the step-up is not a shortcut to M365 E7. It is the full E7 negotiation, conducted entirely on Microsoft’s terms and timeline. It sets the price. It locks in the structure. It establishes the baseline that everything gets measured against for the next renewal cycle. The concessions you secure– or fail to secure—in the step-up define the commercial relationship going forward. Microsoft understands this. The goal of compressing the timeline is to get you to bring step-up energy to what should be a full negotiation event. That asymmetry is not accidental.

The Three Major Step-Up Risks

Three risks deserve attention before any organization signs an M365 E7 step-up amendment.

The first is renewal leverage erosion. Whatever terms you accept today become the baseline Microsoft defends at your next full EA renewal. Pricing, structural provisions, support terms — every concession you give away under time pressure — is a concession that is difficult to recover in the negotiation that follows. A properly scoped E7 engagement would identify and address these leverage points explicitly. A compressed step-up rarely does.

The second is consumption exposure as an unmodeled variable. M365 E7 is a seat-based license sitting on top of a growing layer of Azure consumption meters that are not included in the seat price. A full E7 engagement would include analysis of that consumption exposure, including Azure meter implications, Unified Support cost impact, and protection against future model changes that shift costs from the seat to the meter. A step-up executed under deadline pressure skips that analysis entirely. You are accepting terms without a clear picture of what sits underneath them.

The third is pricing accepted without context. Microsoft evaluates your account holistically. Your Azure consumption trajectory, your Unified Support spend, your on-premises server footprint, your Dynamics investment, your cloud migration roadmap. All of it informs how they price and what they are willing to give. A well-timed M365 E7 decision is a moment to address all of those dimensions simultaneously. A Microsoft Azure Consumption Commitment (MACC) negotiation, a Unified Support restructure, a server licensing conversation. These all have more leverage attached to an E7 commitment than they do standing alone. A step-up amendment executed in thirty days under fiscal year pressure almost never captures that context. You are playing one square while Microsoft is looking at the whole board.

If You Have Not Received a Step-Up Offer Yet: Prepare Now

This is the better position to be in. Use the time.

Understand your current M365 E5 deployment reality before Microsoft does. What is your actual feature adoption across the E5 stack? What is your Copilot rollout status? How many of your users are genuinely positioned to derive value from M365 E7 capabilities today versus in twelve to eighteen months? That data shapes your negotiating position and your ability to push back on a uniform upgrade proposal.

Brief your leadership before Microsoft does. Not to say no to M365 E7, as the technology may well be the right direction, but to ensure that when the conversation happens at the C-suite level, enthusiasm gets channeled into preparation rather than commitment. The best outcome for your organization is a C-suite that says “we want this, let’s make sure we get it right” rather than one that says yes before the right people are in the room.

The step-up is the negotiation. Treating it as anything less is the costliest mistake you can make in the moment.

Take stock of your full Microsoft relationship before the conversation starts. Your Azure trajectory, your Unified Support terms, your on-premises footprint, your cloud migration roadmap. All of it has leverage value attached to an M365 E7 commitment. That leverage disappears the moment you sign a step-up without surfacing it. Do not let the step-up arrive before your preparation does.

If You Have Already Received a Step-Up Offer: Protect What Comes Next

The step-up amendment is coming. The CEO has committed and that is not a conversation you are going to reopen. What you can do is use the window between the handshake and the signature, however wide or narrow that window is, to protect what comes next.

The one thing that matters most is to make sure the step-up is a bridge to a full negotiation, not a replacement for one. That means ensuring the amendment does not automatically carry forward as the baseline for your next full EA renewal without the opportunity to renegotiate. The step-up terms may turn out to be favorable. They may not. What matters is that when your full renewal arrives, you have the right to find out. Not an assumption baked into the amendment that what you signed today is what you are living with tomorrow.

Microsoft may offer pricing protection as part of the step-up, meaning a discount schedule, a price protection clause, and a commitment that sounds generous. Read it carefully. The discount that makes the step-up look attractive today may be engineered to erode on a published timeline while your dependencies harden around the new stack. Directions analyst Steven Kelley examined exactly this mechanism in his recent analysis of Microsoft’s Multiple Equivalent Offer strategy. It is worth reading before you sign anything.

The step-up sets the table. Make sure you still have a seat at it when the full renewal arrives.

Your Move: Sound the Alarm

Spread the word inside your organization before Microsoft spreads theirs. Your IT leadership, your procurement team, your finance partners all need to know the E7 conversation is coming and what it means before it arrives at the C-suite.

The message is simple. This is not about saying no to M365 E7. It is about saying yes the right way, with the right terms, the right protections, and the right to renegotiate when the full renewal arrives.

The step-up is not a shortcut. It is the full E7 negotiation, conducted entirely on Microsoft’s terms and timeline, unless you decide otherwise.

Understanding M365 E7 Series

Part 1: Why E7 Is More Than Just a New Licensing Tier

Part 2: Beware the Step-Up Offer (this article)

In a move some may find surprising — and others not so much — Microsoft plans to make Azure Linux 4.0 a full, commercially available Linux distribution optimized for Azure. Microsoft officials revealed their new plans for Azure Linux on May 18 at the Open Source Summit North America 2026. The company is enabling those interested in test-driving a public preview of it on Azure Virtual Machines to register their interest via a form.

Because everything announced by Microsoft these days is obligated to have an AI angle, Microsoft is positioning Azure Linux 4.0 and the companion Azure Container Linux as a “hardened Linux distribution purpose-built for cloud native and AI workloads.”

Directions on Microsoft had inklings that Microsoft may have been moving to make Azure Linux a full Linux distribution back in 2024. At that time, we noted that Microsoft had no direct competitor to Amazon Linux. And as of April 2024, Microsoft’s LinkedIn division was running an earlier version of Azure Linux internally as a replacement for Red Hat’s CentOS7.

When we asked Microsoft then if Azure Linux might be on its way to full Linux distribution status, a spokesperson told us that “Azure Linux for VM or bare metal use is not available as a commercially supported offering today.”

Two Thirds of Azure Customer Cores Run Linux

Cut to 2026. Microsoft is still saying the majority (two-thirds) of customer cores in Azure run Linux (not Windows Server). Microsoft also says the platforms running Microsoft 365, GitHub and OpenAI’s ChatGPT “all sit on Linux foundations.” Microsoft has supported a wide variety of Linux distributions on Azure for years but never made its own available for commercial use by customers and partners prior to this week’s announcement.

In 2023, Microsoft rebranded its Common Base Linux (CBL)-Mariner distribution as “Azure Linux.” CBL-Mariner is Microsoft’s lightweight Linux distribution designed for Microsoft internal use only in its own first party services and edge-computing appliances. It is the base OS for Azure Kubernetes Service (AKS) container hosts, the base container OS in Azure Stack HCI (now known as Azure Local), and the graphical component of the Windows Subsystem for Linux.

Azure Linux 4.0 is derived from Fedora Linux, with Microsoft curating packages and supply-chain components for Azure. Azure Linux 4.0 will ship as a VM image, with Microsoft officials telling ZDNet that they plan to announce WSL images, as well. However, Microsoft also said there were no plans for Azure Linux 4.0 to be a desktop Linux with a graphical environment.

Update (May 21): For those wondering if they also have the option to install Azure Linux 4.0 on bare-metal servers, the answer is yes, according to a company spokesperson.

“Azure Linux 4.0 is supported across Azure environments, including virtual machines and in Azure products. While it can be installed on bare-metal or outside of Azure, support is focused on cloud-based scenarios,” the spokesperson said, in response to our question.

Microsoft services currently running on Azure Linux 3.0 will transition to the Fedora-derived 4.0 release as it becomes generally available, with ongoing support for 3.0 during a defined transition period.

Azure Container Linux (ACL) is Flatcar Container Linux productized as a hardened, immutable container host that will supersede the AKS host OS based on Azure Linux 3.0.

Microsoft claims this will give developers a more consistent experience, but the move also shows how important and widely-used Linux is within all of Microsoft’s hosted services.

If your Enterprise Agreement is up in the next twelve months, your Microsoft account team is going to put a Multiple Equivalent Offer (MEO) on the table. They will pitch this MEO (sometimes also called Multiple Equivalent Simultaneous Offer) as an upsell that the account team intends for you to perceive as more value at roughly the same cost.

That framing is the bait. It is also a category error. The MEO is not a pricing proposal. It is a leverage-removal mechanism, and the discount you see up front is paying for the disarming of your next renewal — the one after this one — when the price is at its peak in the exit year and your ability to walk away is gone.

What the MEO Actually Looks Like on the Table

Here’s the scenario: The Microsoft pitch deck arrives later than it should, and it’s crunch time with an expiring EA pending. Your team is frustrated and under pressure. Buzzwords appear throughout the deck: Digital Labor, Agentic AI, Frontier Firm, and Copilot Augmentation. They are the tell. Anything good for you, in the account team’s framing, is described in those terms; anything you actually asked for is described as your “historical footprint” and quoted at full Estimated Retail Price (ERP) Level A “equity” pricing, plus the 8%–35% post-July 2026 price increases fully baked in.

Your bill of materials is treated as a curiosity rather than a starting point. The amendment requirements you sent in writing get acknowledged but not addressed. The proposal does not respond to your stated requirements. It responds to the account team’s compensation plan.

Sitting next to that obligatory undiscounted “business as usual” tab are the “rational alternatives.” The MEO arrives with three columns: Your E3 renewal at zero discount, an E5 path at 40% initial discount, and an E7 path at 65%. (If you’re renewing E5, then that gets a goose-egg discount, and E7 is your next Frontier.)

The Year One total of the next higher E-tier is engineered against the price offered on your current estate and lands near your business-as-usual price. E7 lands near it too, just from a higher list price with greater discounts. You are supposed to look at the deck and feel like you have a choice. There are three offers, take your pick, all roughly equivalent at signing.

That equivalency is the first fabrication, and it’s a more sophisticated one than it used to be. The columns aren’t equivalent on any axis except the Year One number, and the Year One number is engineered to be equivalent across all three columns precisely so that the comparison stops there. The MEO’s first letter has come to mean what it says. There really are multiple equal offers now. But the trap they share is singular.

The Year One Math and Why It Is So Seductive

Take the deck at face value for a moment. The displacement story, meaning Microsoft’s pitch to replace an existing third-party solution with one of its own, is real. Defender for Endpoint can replace CrowdStrike. Entra ID P2 can replace Okta. Purview can replace your data loss prevention (DLP), eDiscovery, and records-management stack. Intune can replace your MDM. Mimecast and Zscaler can be rolled into the Microsoft security envelope. The third-party invoices and multiple vendor tentacles go away. As alternate vendor contracts run out, displacement savings, at least on paper, can not only fund the upgrade but eventually may produce a net reduction. Multiply that by five years of declining-but-still-present discount and the spreadsheet is enticing.

It is designed to be. The math is the bait. The point of an MEO is to make the Year One comparison clean enough that procurement can defend the decision in a one-page memo to the C-Suite. The buzzwords do the rest. Nobody at the table wants to be the one responsible for everyone coughing in the wake of the competition’s AI dust cloud.

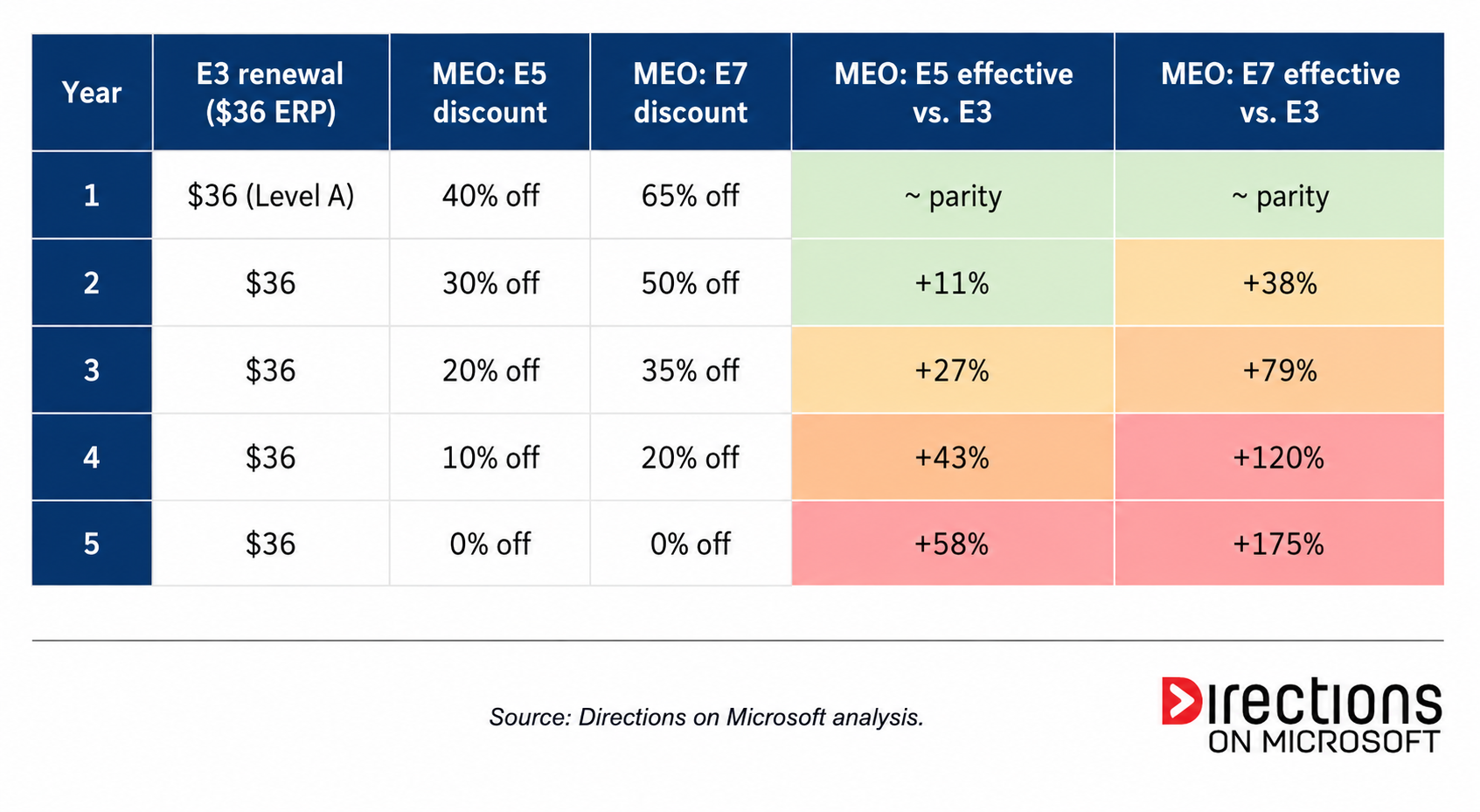

Here is an example of a table the account team will walk you through, missing the last two columns:

The whole proposal paints an ominous trajectory, and the last two columns are where the offers actually balloon. Both MEO paths look like deals in Year One (roughly E3 parity, by design) and both end the term materially above your current E3 ERP. By Year Five, the customer who took the E5 path is paying 58% more than their original E3, fully weaned off of any discount before the renewal even arrives. The customer who took the E7 path is paying 175% more, or almost three times the original E3 ERP, for a footprint they never evaluated on its merits, on a discount scheduled to vanish.

The technobabble is what stays. The deeper the Year One discount, the worse the Year Five reckoning. That is not a coincidence; it is the structure. And then the EA expires, and you renew, which is where the trap closes.

The Dependency Discount: The Contract Microsoft Is Actually Selling

While the bundle ramp is what you see, the dependency discount is what you buy. Each displacement under the MEO does two things at once. It eliminates a third-party vendor alternative, and it hardens a Microsoft-shaped dependency in its place.

Defender for Endpoint displaces CrowdStrike, and your Security Operations Center quietly retools its detection content, IR runbooks, and threat-hunting queries onto Microsoft’s stack. Entra ID P2 displaces Okta, and every SaaS integration in your tenant gets re-federated, and every Conditional Access policy gets reshaped around Microsoft Graph.

Every one of these displacements is defensible in isolation. If your team independently evaluated Defender against CrowdStrike on the merits and chose Defender, that is a legitimate decision. The MEO is not that decision. The MEO is six of those decisions wrapped in a single procurement signature, made simultaneously, on a five-year discount schedule, with no architectural review of the cumulative effect. It is an architectural Trojan horse, infiltrating one quarter at a time, paid for with a discount that erodes on a published schedule while the dependencies harden like curing cement.

It is worth being honest about merit. Defender has come a long way. Entra is fine for most organizations. But the MEO decision is not being made on any of these merits. The bundle is being chosen because it is cheap right now with eye-popping discounts applied, packaged as a single yes. Cheap right now, locked in later is a terrible basis for a decision that will outlast the EA term.

The Trap: The Renewal After This One

Now run the clock forward five years. The discount has eroded over the term to zero. Your renewal quote arrives at full Level A on E5 — or worse on E7. The Year One math that justified the MEO no longer exists. And the leverage you would normally use at this point, basically an assortment of best-of-breed alternative vendors, has been quietly removed during the term you just completed.

You are facing the highest price with the lowest leverage. That is not a coincidence. That is the product. The five-year discount was not a deal. It was the consideration Microsoft paid you to disarm your own negotiation at the renewal after this one. The MEO offers you multiple paths in. The outcome across all of them is singular, and it is not equivalent to anything you would have signed if you had seen it priced honestly.

And do not forget the tax applied to all of this: Unified Support, priced as a rolling 12-month look-back percentage computed against your new EA spend bar. Every dollar you add to the bar as the MEO discount erodes becomes a multiplier on a support contract that you cannot meaningfully decouple.

What Can a Customer Do?

The good news is that the MEO is defeatable, and not all of the moves require executive air cover or a full-blown architectural review board. Some of them just require doing work that procurement teams routinely skip. In rough order of how early in the cycle you should run them:

- Know your personas first

Most enterprises have not done a rigorous license-mix assessment of their actual user population in years, and the MEO works partly because that work always loses to other priorities. The account team is selling you a uniform bundle for all of your users because you can’t articulate why you shouldn’t buy one. If you actually segment your user base into categories like super users, knowledge workers, frontline workers, developers, contractors, you often discover certain combinations of subscriptions that will suffice for certain personas. The bundled MEO is wildly inefficient for that mix, and you cannot demonstrate that to your CFO without the user profiles work. Do this a year before you respond to the MEO, not after. Reconsider Google for your type of frontline workers as the “F3” plan necessitates tenant-wide security and compliance add-ons that catapult F-plans into the $22/month range.

- Reset the “business as usual” baseline before you compare anything

The MEO depends on the business-as-usual column being priced at full Level A so that the discounted alternatives look like deals. Refuse the premise. Demand that your waterfall discount or an equivalent discount off Level A, reflecting your actual volume and tenure, be reinstated on the Business As Usual (BAU) column. Then go further. Argue for renewal pricing that reflects a reasonable uptick over your exit price from the prior agreement, not retail. That is the honest comparison baseline.

This single move does not necessarily collapse the equivalency math. Microsoft can in principle pile enough discount on E5 and E7 to keep the columns aligned. But it forces the account team to decide whether they want to fund the discount levels required to keep the MEO game going against a more honestly priced baseline. Many won’t, because the deal-desk approval threshold for those discounts reaches upper limits, the MEO conversation pivots, and you can bring it back to your particular roadmap requirements. That is the outcome you want.

- For the CIO: Refuse the category

An MEO is not a pricing proposal. It is an architecture proposal with a procurement deadline stapled to it, and it should be evaluated by whoever in your organization actually owns architecture, including your architecture review board, your security architecture function, your enterprise architecture group, whatever it is called. Demand a multi-year total cost model that includes Year Five at full ERP, exit cost, and the cost to rebuild displaced capabilities if you ever need to. If your architecture function would not approve a five-year, six-vendor displacement plan on its merits in any other context, it should not approve it because procurement has a signature deadline.

- For procurement and software asset management: Decouple the displacements

Each displacement is its own decision, with its own business case, its own timeline, its own Proof of Concept, and its own contract. Do not let a bundle discount paper over numerous independent vendor evaluations. Stagger your third-party renewal dates so that at the next EA, at least some of those alternatives are live, contracted, and ready to scale and are not just theoretical. Model the exit cost from Microsoft alongside the entry price into Microsoft, because the cheapest deal at signing is the most expensive deal at the next renewal if you cannot credibly walk away.

- If you are signing anyway, negotiate the erosion rate and demand a Not-to-Exceed

Some MEOs will get signed regardless of what is in the prior four sections because procurement was overwhelmed, the persona work didn’t get done, the architecture function wasn’t asked in time, or, most commonly, leadership rests securely that “nobody got fired for buying the whole Microsoft stack” and the MEO is the path of least organizational resistance. If that is your situation, the conversation shifts from refocusing the requirements conversation to harm reduction, and there are still two contractual moves worth making.

First, negotiate the erosion rate. The 40 / 30 / 20 / 10 / 0 schedule (or its E7 equivalent) is a starting point computed on equivalency declining to zero over the term; it is a structure the account team proposed because it maximizes the trap. Argue for a flatter curve, which means a sustained discount across the term, ideally one that does not fully decay, or anchor on a flat discount for the full term, given some amount of determined value is indeed present.

Second, and more importantly, insist on a Not-to-Exceed (NTE) cap on the subsequent renewal, written into this contract. The NTE should contractually limit how much the per-user price can move at the renewal after the MEO term ends, capped at a small premium on the exit price and written very meticulously. This is the single contractual provision that directly addresses the thesis of this piece. It does not eliminate the dependency hardening, but it removes the pricing power that the MEO discount table was buying Microsoft.

If Microsoft refuses the NTE, that refusal is meaningful. Document it, escalate it to your executive sponsor, and use it. An account team unwilling to commit to bounded pricing at the next renewal is telling you what they intend to do at the next renewal, and you have just witnessed how that works.

The Discount Is Real; The Trap Is Real

The MEO is a playbook owned by Microsoft’s Sales Excellence organization, and it is being run on every enterprise renewal in FY27. The discount is real. The trap is real. Both are true at the same time, and a customer who only sees one of them is going to sign a deal whose true cost does not arrive until that next EA is on the horizon.

The work required by you is unglamorous: Persona analysis, baseline resets, architecture reviews, contract clauses. None of it is rhetorically satisfying. But all of it is the difference between signing a five-year discount and signing the disarmament of your next negotiation.

Don’t get defanged. A Directions on Microsoft advisor brings the persona analysis, the architectural lens, and the negotiation playbook to the conversation before the MEO does.

Microsoft 365 used to be one bill. It isn’t anymore.

Most organizations treat their Enterprise Agreement (EA) and their Azure agreement as two separate ledgers. Different contracts, different cycles, different teams with different skills. But no one designed that separation. It was the natural outcome of two agreements that evolved independently while the workloads beneath them quietly converged.

A growing share of what your organization actually consumes from Microsoft 365, particularly its security, compliance, analytics, and AI workloads, no longer bills against the M365 invoice at all. It bills against your Azure agreement, on a meter, by usage. Some of it always did. A great deal more of it now does or will soon. And almost none of it surfaces in the EA negotiation.

This is not a future trend. It is current, structural, and accelerating. Without a common framework that spans both agreements, organizations cannot see their true M365 footprint. What they cannot see, they cannot negotiate.

The Cost Reduction That Isn’t

Consider a scenario nearly every large Microsoft 365 customer goes through at some point.

Power BI Premium, historically purchased as P-SKUs on the EA, is being phased out and replaced by Microsoft Fabric capacities. The replacement F-SKUs bill as Azure consumption, not as a defined EA license. Microsoft will tell you that Fabric capacity under Azure offers more flexibility than the P-SKUs it replaces. You can pause your capacity when you don’t need it, scale up when you do, and reserved instances offer built-in discounts to help lower the cost. That framing is accurate as far as it goes.

What it doesn’t say is that even with reserved instance discounts, Fabric capacity is meaningfully more expensive than the Power BI Premium it replaces. When the P-SKU drops off the EA, that line item disappears cleanly from the EA bottom line. When the F-SKU lands in Azure, it lands at a higher number. The Azure bill rises by more than the EA bill fell. Across both ledgers the organization is paying more. The EA renewal will be negotiated against a number that no longer reflects the full picture.

This isn’t a cost reduction. It’s a cost migration, and a more expensive one. Every cost migration from your EA to your Azure agreement also weakens the baseline you will defend at your next EA renewal, because the EA renewal is sized against EA spend, not total Microsoft spend.

What Else Is Hiding in Your Azure Bill?

Power BI to Fabric is the most visible example. It is far from the only one. The categories below all bill on the Azure side already, and most large EA estates have exposure to several of them today.

Microsoft Sentinel and Azure Monitor. Microsoft 365 E5 includes a Sentinel data ingestion benefit, but it is a dollar-value credit, not unlimited capacity. The standard M365 security and audit data fits inside the credit. Anything beyond that meters fully against Azure: additional log sources, longer retention, advanced analytics, and any M365 data routed into Log Analytics for compliance reporting. Mature security programs routinely overshoot the entitlement, sometimes by an order of magnitude. Organizations that assumed E5 had this covered find out otherwise from the Azure bill.

Microsoft Purview. Several Purview capabilities, particularly the newer Data Governance and Data Security functions, have shifted to Azure consumption pricing layered on top of the E5 Compliance entitlement. The licensed seat gets you baseline access. Heavy scanning, classification, and analytics meter against Azure.